Financial scenario planning helps businesses prepare for different futures by modeling potential outcomes like growth, decline, or stability. Unlike forecasting, which predicts a single outcome, this approach examines multiple possibilities, enabling businesses to make informed decisions in uncertain conditions.

Key Highlights:

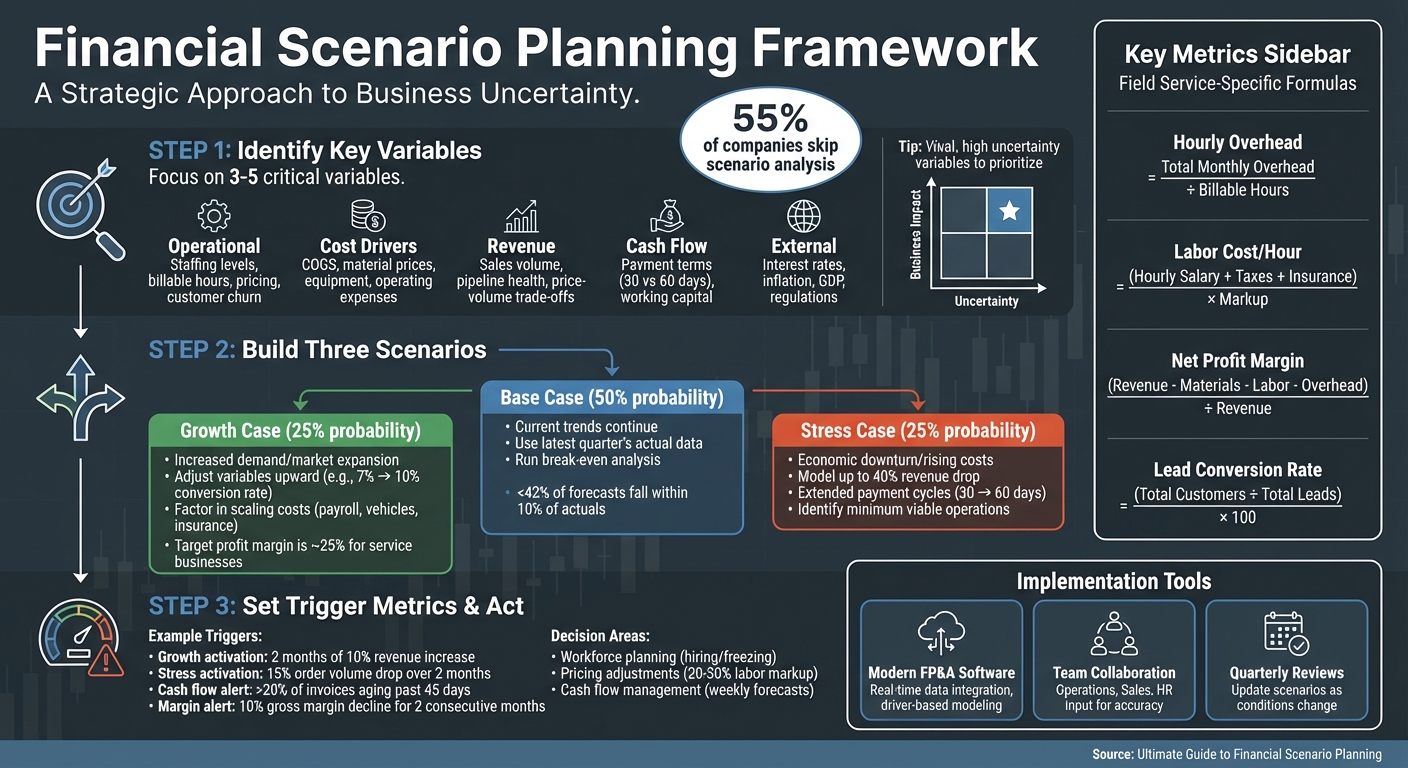

- Why It Matters: Over 55% of companies skip scenario analysis, leaving them unprepared for market shifts.

- Who Benefits: Service businesses, particularly those with fluctuating cash flow, seasonal demand, or rising costs.

- Core Steps:

- Identify key financial variables (e.g., labor costs, sales volume, customer churn).

- Build three scenarios: base (current trends), growth (optimistic), and stress (challenging conditions).

- Use these scenarios to guide decisions on hiring, pricing, and cash flow.

- Actionable Tools: Set "trigger metrics" (e.g., a 15% drop in orders) to signal when to act.

Financial Scenario Planning Framework: 3-Step Process for Service Businesses

Core Elements of Financial Scenario Planning

Identifying Your Most Important Variables

Start by pinpointing 3–5 critical variables, both within your control and external, that heavily influence your financial performance.

For operational factors, consider elements like staffing levels, billable hours, pricing approaches, and customer churn rates. On the cost side, focus on drivers such as your cost of goods sold (COGS), raw material price fluctuations, equipment investments, and ongoing operating expenses. Revenue drivers include sales volume, the health of your sales pipeline, and the price vs. volume trade-off, aka how pricing adjustments could impact total sales.

Cash flow is another key area. For instance, extending accounts receivable terms from 30 to 60 days can directly affect your working capital. External factors like interest rate changes, inflation, GDP growth, and new regulations also play a role. If you've heard of the PESTLE framework for external factors, it can be useful. PESTLE stands for Political, Economic, Social, Technological, Legal, and Environmental. Thinking in this structured way makes sure you account for the biggest external influences. Additionally, a simple 2x2 grid that maps variables by "Business Impact" and "Uncertainty" can help prioritize high-impact, high-uncertainty factors.

These variables serve as the foundation for building your financial models.

Building Your Financial Models

A driver-based approach is a great starting point. Use historical data to determine how changes in key drivers affect your financial outcomes. Include calculations for fully burdened labor rates and hourly overhead to ensure accuracy.

To calculate hourly overhead, divide your total monthly overhead by billable hours. Fully burdened labor rates should include hourly wages, workers' compensation, taxes, and benefits. You could also include training and certification budgets, laptops or tablets, phones, and software licenses required for that position.

The goal of these models isn't to find a single "right" answer. Instead, it's to help inform the C-suite, so decisions are grounded in basic financial logic and not a gut-level guess.

Develop three key scenarios for planning: a low case (worst-case scenario with declining revenue), a medium case (status quo), and a high case (best-case scenario with increased demand). Running a break-even analysis will help determine the sales volume required for each scenario. Your models should reflect realistic expectations of both revenue and profit based on your service business.

Field Service-Specific Metrics to Track

Once your models are in place, focus on metrics that inform operational decisions. Metrics like the ratio of billable to non-billable hours are crucial for understanding labor efficiency.

Labor cost per hour can be calculated using this formula: (Hourly Salary + Taxes + Insurance) x Markup.

To measure profitability, use the net profit margin formula: (Total Revenue - Materials - Labor - Overhead) ÷ Total Revenue.

To track lead conversion rates, use this formula: (Total customers ÷ total leads) x 100.

This data can help you assess the impact of marketing efforts or sales process improvements. Additionally, account for vehicle and equipment maintenance costs, which can fluctuate unexpectedly and should be included in stress-test scenarios.

Lastly, establish trigger metrics to signal when it's time to shift strategies. For example, if order volume drops by 15% over two consecutive months, it might be time to activate your stress response plan. Similarly, monitor technician turnover or spikes in material costs, and set specific thresholds that would require a reevaluation of your financial approach.

Creating Your 3 Core Scenarios

Scenario 1: Base Case

The base case scenario is essentially your "business as usual" forecast - the most likely outcome if current trends continue without any major shifts.

To start, use your latest quarter's actual performance data. Pull key metrics for your professional services business like net promoter score, average job value, operating and labor costs. This data establishes a clear picture of what "normal" looks like for your business. Then, focus on identifying three to five key variables that drive your financial outcomes, such as technician utilization rates or accounts receivable (A/R) / day sales outstanding (DSO).

Assign this scenario a 50% probability of occurring. Alongside the numbers, include a concise narrative that explains the assumptions and growth expectations behind your forecast. To ensure your baseline is viable, run a break-even analysis to calculate the minimum sales volume needed to keep operations running smoothly.

Keep in mind that financial forecasts are rarely spot-on. It could be off by 10%; it could be off by 25%. While your base case won’t be perfect, it serves as the benchmark for evaluating other scenarios.

Once you’ve established your baseline, you can start exploring the potential for growth.

Scenario 2: Growth Case

The growth scenario is where you map out the upside. What happens if demand surges, you expand into new markets, or your marketing campaigns deliver better-than-expected results? Assign this scenario a 25% probability.

The simplest way to create your growth scenario is to take your base case model and adjust key variables upward. For instance, if your base case assumes a 7% lead conversion rate, you might project a 10% rate for the growth scenario, factoring in increased marketing spend. Similarly, if you plan to hire more technicians, calculate the added revenue potential alongside higher payroll, vehicle, and insurance costs.

Work backward from a revenue target using normative planning. Say you aim to 1.5x revenue in 24 months, you'll break that goal into actionable steps, like increasing weekly job volume, boosting ticket sizes, or expanding your fleet. Collaborate with your sales and operations teams to validate these assumptions, shifting the focus from debating numbers to addressing real challenges.

Set specific triggers that activate your growth strategy. For example, two straight months of 10% revenue growth above projections could signal it’s time to hire more staff or invest in new equipment. As you scale, make sure your profit margins stay healthy.

With the growth path mapped out, it’s time to prepare for tougher scenarios.

Scenario 3: Stress Case

The stress scenario helps you plan for rough waters. It's not a matter of if you'll experience them; it's a matter of when. Whether it’s an economic downturn, supply chain disruptions, or rising costs that squeeze your margins. Like the growth scenario, assign this one a 25% probability.

Start by modeling external pressures, such as inflation, regulatory changes, or rising interest rates. Then factor in operational challenges, like supply chain delays or reduced workforce availability. For instance, if a competitor enters your market, your cost per lead might jump from $150 to $250, while conversion rates could drop from 7% to 4%.

Expect changes in customer behavior too. During challenging times, customers may downgrade to cheaper services, churn rates might increase, and payment cycles could slow. Plan for extended payment terms (maybe moving from 30 to 60 days) and account for the strain this puts on working capital.

Establish triggers, such as a 15% drop in orders over two months or more than 20% of invoices aging past 45 days. Run a break-even analysis to determine the absolute minimum sales volume required to stay afloat, and identify variable costs you can cut immediately, like discretionary spending, overtime, or new hires.

Model worst-case revenue drops of up to 40% and limited access to credit. The goal isn’t to predict disaster but to ensure you have a plan in place to extend your financial runway if conditions worsen. This way, you’re prepared to act quickly and decisively.

Scenario Planning for Small Business Survival | Cash Flow Forecasting Walkthrough

Here's a solid video on this topic, if you're wanting to see a walkthrough of how to do financial scenario planning.

Turning Scenarios Into Business Decisions

Once you’ve built your financial models, the next step is to use them for decision-making. These scenarios are theoretical, yes. But they’re tools to guide real business actions too, from hiring to pricing and cash flow strategies.

Workforce Planning and Hiring Decisions

Don’t wait for staffing issues to arise. Use scenario planning to guide proactive hiring decisions.

For example, set clear performance or revenue milestones to determine when it’s time to expand your team. If revenue consistently exceeds expectations for several months, it might signal the need to hire additional technicians. When planning for new hires, factor in all costs, including salary, benefits, equipment, and training, to avoid surprises. You should know what it costs to hire a new tech vs. hire a new dispatcher vs. a new field service manager.

In challenging scenarios, define triggers like falling gross margins or an increase in overdue invoices to pause hiring, freeze bonuses, or reduce contractor hours. Losing key employees can be costly not just in recruitment fees (estimated at $35,000 for a pivotal manager) but also in delayed revenue, which could amount to $200,000+. To mitigate risks, focus on cross-training and succession planning.

Driver-based modeling can also help align staffing with workload. For instance, if data shows each technician can handle a specific number of service calls, you'll want to use this to adjust your team size based on projected call volumes.

Adjusting Pricing and Margins

Scenario planning can also reveal when it’s time to tweak your pricing strategy. Service businesses often rely on labor markups of 20–30% to achieve a their desired net profit margin.

Start by calculating your hourly overhead. Divide your monthly overhead by billable hours to determine the minimum cost per hour you need to recover before turning a profit. Add labor burden rate as we outlined in a previous section above, and apply a markup to set a sustainable rate.

In tough times, monitor key indicators like rising material costs or declining order volumes. If raw material prices spike, review job pricing to decide whether to absorb the cost, pass it on to customers, or find efficiencies elsewhere.

Consider hybrid pricing models to stay flexible. For example, use flat rates for routine work like maintenance, and time-and-materials pricing for complex or emergency jobs. Be cautious with discounts. If they cut too deeply into margins, focus on offering discounted upsells instead.

Finally, use your financial software to set alerts for key variables like inflation or cost increases. These alerts can help you adjust pricing before margins take a hit.

Managing Cash Flow

Scenarios can also help you pinpoint the break-even sales volumes needed to maintain cash flow. Knowing this threshold is critical during uncertain times.

During periods of volatility, switch to weekly cash forecasts to keep a close eye on collections and overdue payments. For instance, one service provider used weekly cash forecasts during an economic downturn to monitor revenue, cut discretionary expenses, and pause hiring, which helped extend their cash reserves.

If payment cycles start to stretch, calculate the resulting cash gap and plan for additional working capital or financing. Rapid growth can also strain cash flow, as expenses like payroll and materials often increase before customer payments come in. To manage this, calculate your cash conversion cycle and set triggers for action. For example, if receivables over 45 days exceed 20% of your total, tighten your collections process immediately.

Tools and Methods for Scenario Planning

Once you've laid the groundwork with solid models, the right tools and methods can make your scenario planning process faster and more effective.

Use Financial Planning Tools

Relying on traditional spreadsheets like Excel can hold you back. Although familiar, spreadsheets often create version control headaches, which can slow you down when quick decisions are critical. Modern financial planning platforms solve this issue by providing real-time data, eliminating delays caused by manual updates. Financial data in spreadsheets can also be spread out across multiple files, whereas financial planning software can integrate all in one place.

These advanced tools use driver-based modeling, allowing you to tweak key variables and immediately see how they affect revenue and cash flow. Some even go a step further with multi-dimensional reporting, letting you break down financial data by region, technician, or service line. This level of detail helps you identify exactly where events are impacting your bottom line.

Getting Your Team Involved

Scenario planning works best when it's a team effort. If you build scenarios in isolation, you risk creating plans that don't align with operational realities. Bringing in leaders from operations, sales, and HR ensures that your financial assumptions reflect what's happening on the ground.

This collaborative approach not only improves accuracy but also fosters buy-in. When department heads help shape assumptions and set clear triggers, like a 10% drop in gross margins over two months, they're more likely to act decisively when those triggers are hit.

To avoid overcomplicating things, focus on just the three primary scenarios and the key variables that drive major changes. Build clear narratives around each scenario so non-financial stakeholders can easily grasp the story behind the numbers.

Updating Your Scenarios Regularly

Scenario planning isn't a one-and-done task. Markets and industries change constantly, so your scenarios need to keep up. Treat your forecasts as living documents, revisiting them quarterly or whenever major external factors shift.

Set clear triggers to prompt reviews. For instance, if gross margins drop by 10% for two consecutive months, it might be time to reassess your assumptions and activate a stress-case plan. Modern financial software can even use AI to detect these changes automatically, reducing the need for constant manual checks.

Connecting your planning platform to systems like ERP, CRM, and payroll ensures your data updates automatically. This enables agile, rolling forecasts that reflect your current trajectory.

Additionally, conducting quarterly PESTLE reviews (Political, Economic, Social, Technological, Legal, Environmental) helps you anticipate external risks before they escalate. Regular updates to your scenarios ensure your strategy remains aligned with real-time financial and operational shifts, empowering you to make informed decisions swiftly as conditions change.

Conclusion

This guide has shown how scenario planning can act as a safety net for your business. Financial scenario planning helps service businesses prepare for a variety of potential futures. Interestingly, most service companies still skip scenario analysis when adjusting forecasts. But those service businesses that do embrace it gain a clear edge by having actionable plans ready to tackle unexpected market shifts. It turns uncertainty into clarity and allows you to be poised when others panic.

By modeling Base, Growth, and Stress cases, you can safeguard cash flow, scale with confidence, and make quicker decisions. Setting specific financial triggers ensures you know exactly when to implement each plan. Plus, involving your operations, sales, and HR teams in building assumptions and defining these triggers builds their commitment to executing the plan when the time comes.

Getting Started

Now that you understand the benefits, it’s time to turn theory into practice. Start small: use your existing financial data to create three core scenarios. Your Base Case should reflect current trends, the Stress Case should test your cash flow under challenging conditions, and the Growth Case should map out how to scale while protecting margins. Focus on just three to five key metrics, like burden rate, customer churn, and average job value.

If you're looking for tools to help you get started, our free resources here at Service Empire AI are tailored for field service businesses. These include financial scorecards, break-even analysis templates, and pricing scripts created by entrepreneurs who’ve scaled their businesses to nine figures.

Set a quarterly schedule to review and update your scenarios as market conditions shift. Clearly define the triggers that indicate when it’s time to move from one plan to another. The companies that succeed in uncertain times aren’t the ones with flawless predictions; they’re the ones that have already thought through their options and are ready to act.

FAQs

What financial factors should I focus on during scenario planning?

When diving into financial scenario planning, it's crucial to zero in on the variables that can heavily influence your business's performance. Some of the most important ones to keep an eye on are:

- sales projections

- cash flow

- operating expenses

- employee headcount

- raw material costs

- market trends

Carefully examining these elements allows you to anticipate potential hurdles, spot growth opportunities, and make smarter decisions. This approach helps your business stay adaptable and prepared, no matter what challenges come your way.

How does scenario planning help businesses make better decisions during uncertain times?

Scenario planning allows businesses to prepare for uncertainty by considering various potential outcomes. This approach helps leaders foresee challenges, spot opportunities, and create strategies to manage different situations well. By addressing risks ahead of time and organizing resources strategically, companies can make well-informed decisions that boost their adaptability and ensure steady growth over time.

What tools can service businesses use for financial scenario planning?

Planning for various financial outcomes is much easier when you have the right tools to model and forecast. Today, specialized software platforms make it possible for businesses to craft multiple scenarios, analyze live data, and prepare for uncertainties. Features like automated forecasting, customizable financial models, and scenario comparisons empower service businesses to make smarter, data-driven decisions.

For smaller businesses or those just dipping their toes into scenario planning, spreadsheets can be a great starting point. By tweaking assumptions on income statements to reflect best-case, worst-case, and most likely outcomes, you can build a reliable starting framework. That said, advanced software designed specifically for service businesses can take your planning to the next level. These tools improve accuracy and streamline the process, helping business owners forecast sales, cash flow, and other key metrics with greater confidence.

Stop Wasting Time on Plans That Never Get Executed